Last updated: July 7, 2026 · Prices reviewed quarterly

The rule insurers actually apply: sudden and accidental water damage is covered; gradual damage and outside flooding are not. The average paid water claim runs $13,954 (Insurance Information Institute, 2018-2022 water damage & freezing claims) — but plenty of legitimate-sounding claims get denied for reasons you can avoid.

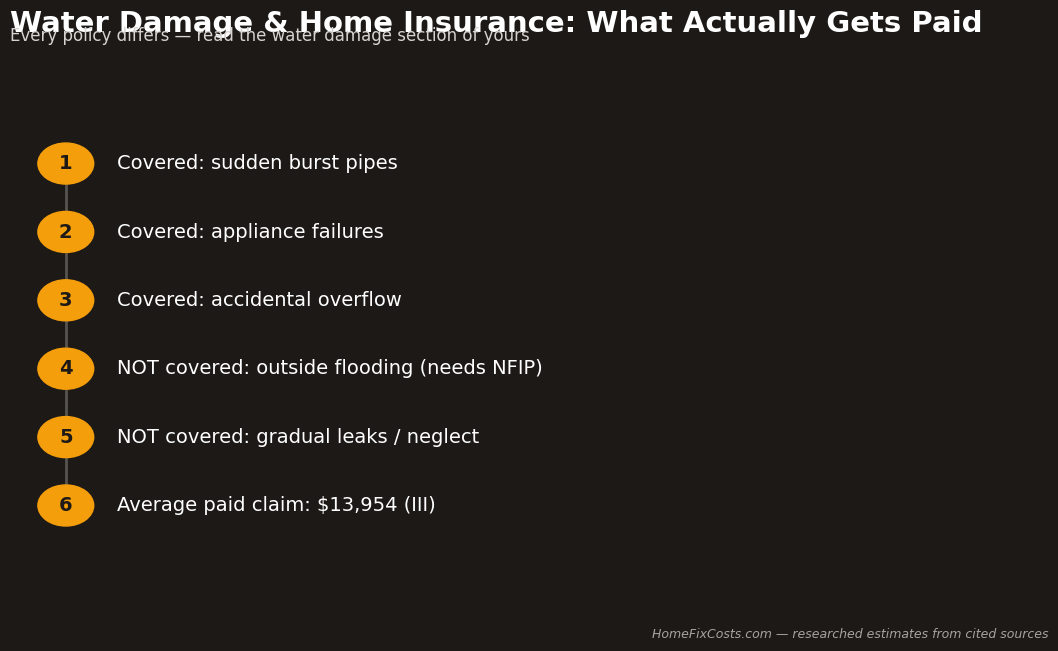

Covered vs. not covered

| Usually COVERED (sudden/accidental) | Usually NOT covered |

|---|---|

| Burst or frozen pipes | Flooding from rain, rivers, storm surge (needs separate NFIP/flood policy) |

| Washing machine / water heater failure | Gradual leaks you “should have known about” |

| Accidental tub or sink overflow | Poor maintenance (old roof, failing caulk) |

| Roof leak from a storm-created opening | Sewer backup (needs an endorsement rider) |

| Firefighting water | Groundwater seepage |

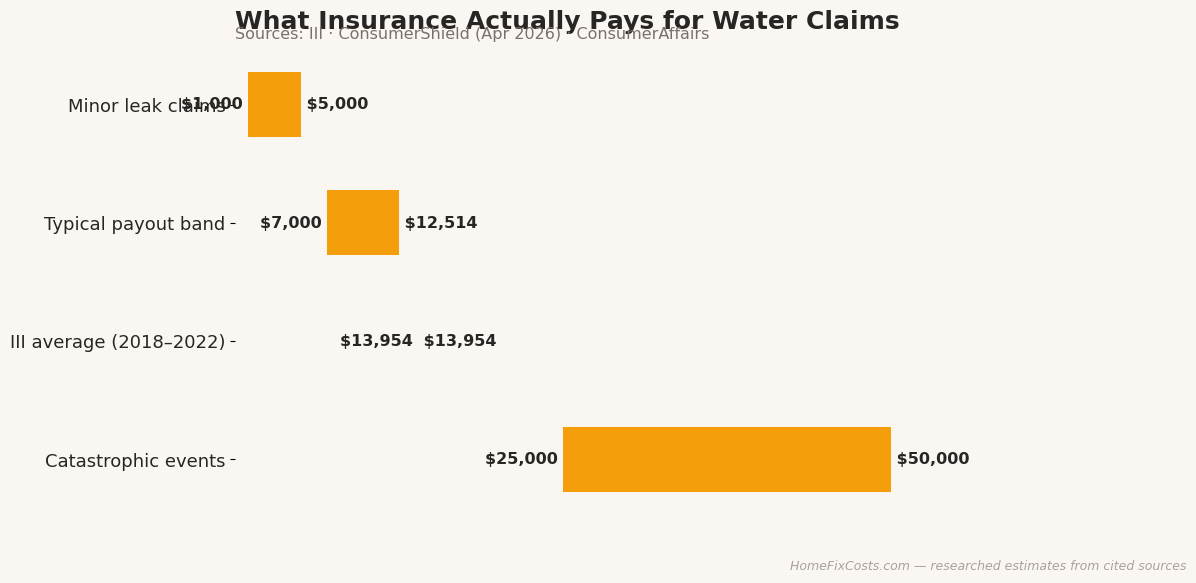

What a real payout looks like

Payouts range from about $1,000 for minor leaks to $50,000+ for catastrophic events, with typical checks in the $7,000-$12,500 band (2026 estimates) and the III average at $13,954. The insurer pays actual repair cost minus your deductible — and disputes usually center on scope (how much drywall, whose square footage) rather than yes/no coverage.

The 6 moves that protect your claim

1) Stop the water and photograph everything BEFORE cleanup. 2) Report within 24-48 hours. 3) Make only reasonable temporary repairs (tarp, shutoff) and keep receipts — insurers must pay reasonable mitigation. 4) Do not let a restoration company “handle the insurance” before reading their contract; assignment-of-benefits abuse is real. 5) Get your own contractor quote to counter a thin adjuster estimate (what jobs really cost). 6) Denied as “gradual damage”? Demand the denial in writing and escalate — resources below.

Flood is a separate universe

No standard homeowners policy covers rising outside water. FEMA’s National Flood Insurance Program (NFIP) and private flood carriers do, with a typical 30-day waiting period. Anywhere near a flood zone, price it before the season at FloodSmart.gov.

Official resources & free help

- Flood coverage (separate policy): FloodSmart.gov — NFIP, FEMA

- Claim denied or stalled: your state insurance department via NAIC consumer resources — complaints are free and get responses

- Declared disasters: DisasterAssistance.gov · FEMA 1-800-621-3362

- Claim statistics & consumer guides: III.org

- Free legal aid for coverage fights: LSC.gov

FAQ

The adjuster says my pipe leak was “long-term.”

Ask for the moisture or engineering evidence in writing, then counter with your plumber’s causation statement. “Gradual” is the most-abused denial reason — and the most reversible.

Will a water claim raise my premium?

Often at renewal, and multiple water claims can trigger non-renewal. For damage barely above the deductible, do the math before filing.

Is mold after the leak covered?

If it flows from a covered sudden loss, usually yes but often capped ($1,000-$10,000 by policy). Details: mold removal costs.

Prices on this page are researched estimates compiled from the cited sources; your local costs will vary with market, access and scope. Always get multiple written quotes from licensed professionals before hiring.